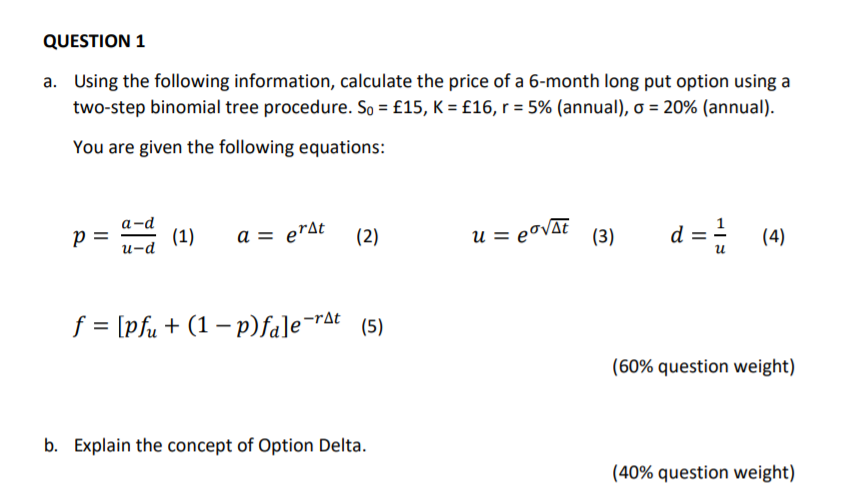

QUESTION 1 a. Using the following information, calculate the price of a 6-month long put...

60.1K

Verified Solution

Link Copied!

Question

Finance

QUESTION 1 a. Using the following information, calculate the price of a 6-month long put option using a two-step binomial tree procedure. So = 15, K = 16, r = 5% (annual), o = 20% (annual). You are given the following equations: a-d u-d (1) a = erat (2) u = eovat (3) d = (4) f = [pfu + (1 - p)fale-rat (5) (60% question weight) b. Explain the concept of Option Delta. (40% question weight)

Answer & Explanation

Solved by verified expert

Get Answers to Unlimited Questions

Join us to gain access to millions of questions and expert answers. Enjoy exclusive benefits tailored just for you!

Membership Benefits:

Unlimited Question Access with detailed Answers

Zin AI - 3 Million Words

10 Dall-E 3 Images

20 Plot Generations

Conversation with Dialogue Memory

No Ads, Ever!

Access to Our Best AI Platform: Zin AI - Your personal assistant for all your inquiries!